Let's Get You Into A House - Strategies 3 & 4

Budgeting strategies to get yourself into a home. We've been considering the steps that people go through mentally to get ready to buy a home. And they normally ask themselves a bunch of questions, which as it turns out, are the same questions financial planners and mortgage brokers ask, or at least should be asking their potential clients. These questions are (1) Financially speaking, where are you?, (2) Financially speaking, where do you want to be?, and (3) Again financially speaking, how are you going to get where you want to go? And of course, in the context of this blog, "where you want to go" refers to buying a home.

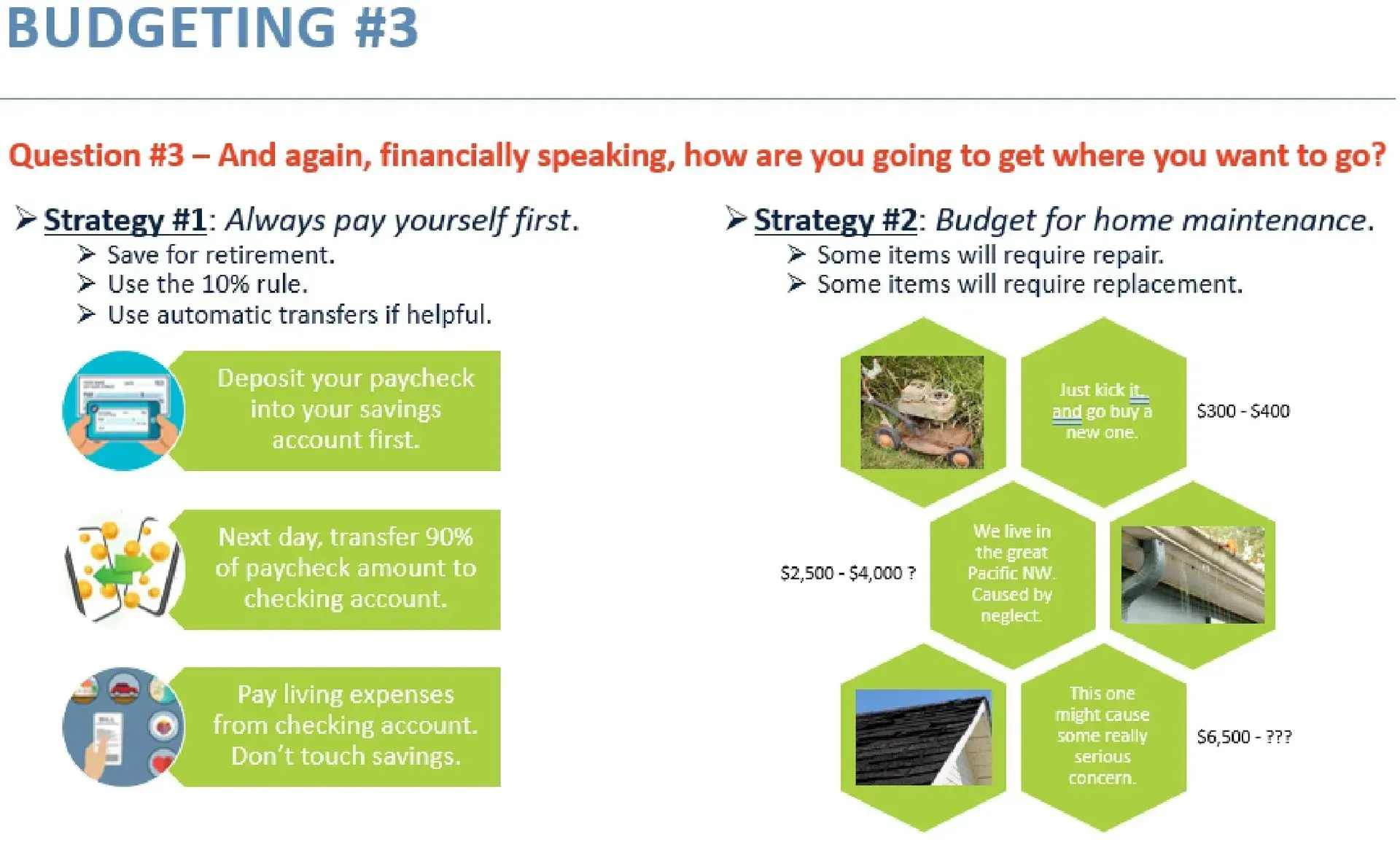

Last week we began to look at some specific strategies that are often suggested to help homebuyers reach their goal. The first was to "Always pay yourself first" by saving 10% of what you earn. The second was to budget a little bit for home maintenance every month, because in some ways, houses are like cars. Parts wear out, and either need to be repaired or replaced, and with a house, those parts can be quite expensive, and you don't want to be caught unaware. This week we're going to look at the next two strategies which can be utilized to help you ready yourself to buy a home.

Strategy #3

is to start living as if you already have a mortgage, and here's how it works. Let's say you're already paying $2,000/mo. for rent, and you're concerned as to whether or not you can actually afford a mortgage. First, select a neighborhood where you'd like to live, and actually write down on paper what you need in a home. Then contact your real estate broker, and ask what such a home would actually cost. Once you have a price range in mind, contact your mortgage broker, and find out what a mortgage payment would be on such a home. For the purposes of this scenario, let's say that payment comes to $3,400/mo. for principal, interest, taxes, insurance and mortgage insurance. That's a $1,400 increase, and you might be worried whether or not you can sustain that over a long period of time - perfectly understandable, right? The way to determine whether or not you can sustain it is to go ahead and pay your $2,000 monthly rent, AND save $1,400 each month, in a separate savings account, designated for your closing costs when you buy your home. Do this for 3 months, 6 months, maybe even a year. Take however long you need. At the end of this time, you will know whether or not you can actually do it, and you'll make the appropriate decision.

Strategy #4

is to minimize credit card debt. Mismanagement, and in some cases non-management of credit card debt kill more mortgage applications than anything else I see. So it's critical to understand how this can affect you when applying for a mortgage. It's actually a subject unto itself, and it's too long to go into real depth here, but I can at least give you some time-tested methods to manage a situation that's tough for many people. First, list out all your credit card accounts, their balances, their limits, and their interest rates. Sort them by balances owed first, and secondly by interest rate. Second, starting with the balances that are easiest to do this with, pay each of the cards' balances down to 50% of their limits, and NEVER exceed 50% again. Most people do not understand that when they exceed 50% of a credit card's limit, it begins to lower their credit scores. Once you've accomplished this, pay them down to 30% of their limits, and NEVER exceed 30% again. If you do this, you'll begin to see rapid increases in your mortgage credit scores. But hold on - you're not done yet.

Next, use each card you have periodically. The reason for this is that banks who issue credit cards are in business to make money. If you don't charge something periodically, they won't make any money, and eventually they will close the credit card account for non-use. And this will lower your credit score for a couple reasons which are too detailed for this blog. Just be sure you use each card you have... You don't have to use each one every month, but use each one every few months, even if it's just for a tank of gas in your car.

Last - never close a credit card account! There are two exceptions to this. If your identity has been hacked and you fear that someone may have gotten your credit card information, call the bank who issued you the card, and have them issue you a new card. And if for some reason you suspect that the bank who issued you the card is going to close the account for non-use, either charge something on it immediately, or close the account yourself. It always looks better on a credit report if you've closed an account, than if the creditor closes the account on you.

Hopefully the questions we've looked at, and the strategies that I've suggested are things you find helpful as you get ready to buy your home. If you have questions about any of it, please feel free to

reach out to me at anytime. Remember, I don't work 9-5, I work start-to-finish, and I will always give you straight talk without any sales talk.

Home Mortgage Loan Reviews

Browse My Website

Contact Information

Phone: (425) 210-2963

Email: jeyre@nexamortgage.com

Operating From 13320 Hwy 99, Unit 197, Everett, WA 98204

License: NMLS #442452

Corporate NMLS # 1660690

Business Hours

Mon - Sat: 8:00 am - 7:00 pm

Sunday: 4:00 pm - 7:00 pm

Corporate Address: 3100 W Ray Road, #201, Office 209, Chandler, AZ 85226